Dedicated Fintech Software Development Company

We build financial apps with a strong understanding of industry regulations and a deep commitment to security and compliance.

Trading Software Development Services

Craft intuitive trading platforms for diverse financial assets, providing seamless transactions and real-time analytics to boost trading experiences.

Insurance Software Development Services

Tailored insurance software solutions, optimizing underwriting, claims processing, policy management, and risk assessment.

Custom Banking Software Development

Modernize banking services through mobile apps and blockchain integration. Improve customer experiences while maintaining security.

Custom Financial Software Development

AI, no-code, low-code - we create custom financial software solutions that match the needs of both fintech startups and well-established financial institutions.

Custom Mobile Banking App Development

Build a cutting-edge mobile banking app with seasoned fintech developers and UX designers. Leverage our decade of experience.

Accounting Software Development Services

Save time and money by automating book keeping processes in your business. General ledger solutions, inventory management platforms & more.

Custom Blockchain Development Services

Everything you need

to build blockchain products in one place:

New blockchains, smart contracts, tokens, NFT, cryptocurrency exchanges.

Custom Asset Management Software

Create investment solutions that boost revenue and ease wealth management. Expertly designed to meet your financial goals.

NFT Trading Platforms Development

Lead in the realm of digital assets with secure, scalable, and user-centric NFT exchange platforms. Liquidity, performance, and regulatory adherence.

Custom Lending Software Development

Streamline lending operations and empower borrowers with custom loan origination systems, credit risk management, and tracking systems.

Digital Wallet App Development Services

Secure, trusted mobile and web e-wallet solutions for businesses & their clients. Convenient payments at your fingertips!

Payment Gateway Integration Services

Protect your business with our secure payment gateway integration services. Accept payments from all major credit cards and debit cards.

Bloc-X: A new way to trade commodities

Bloc-X is an OTC trading platform for Oil Blocs Future markets. Independent, fully compliant and regulated platform that connects ICE, NYMEX and SGX.

Read Case Study

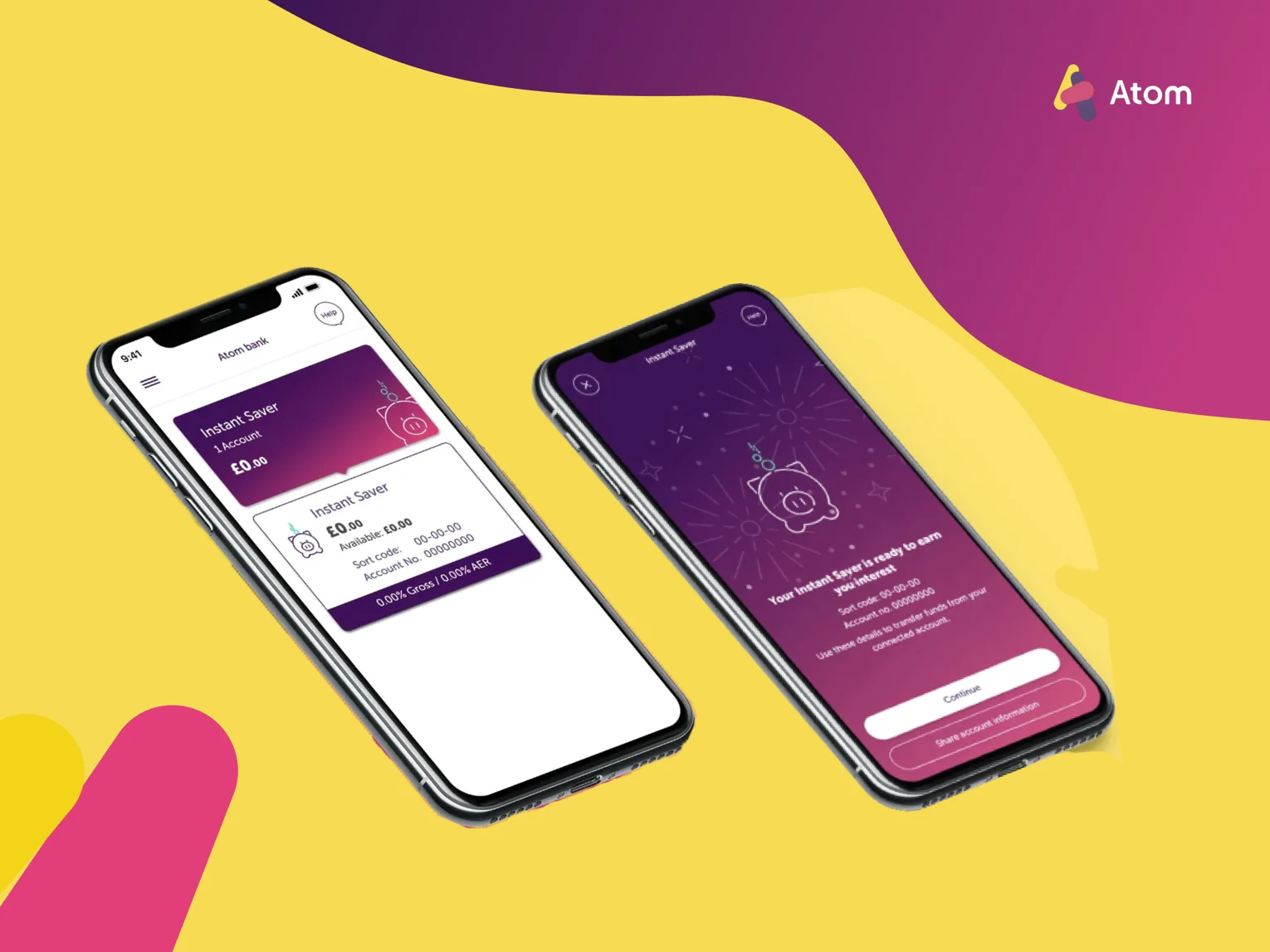

Atom Bank: Establishing an entirely new, remote team for the UK’s first fully digital bank

Atom Bank was looking for a solution that could increase their ability to deliver business changes fast. We've provided experienced, high-quality programmers to complement the existing UK team and add engineering capacity.

Read Case Study

KodyPay: Scaling a software development team for one of the best mobile payment startups

Back in 2022, KodyPay faced a shortage of skillful developers in the UK pool and high salary requirements in its sector.

Thanks to Poland's competitive developer rates & high expertise, we helped them scale their existing team in Berkshire and improved the development process.

Read the case study

What stands out about working with Pragmatic Coders is the trust we can place in the team. They provide helpful estimates, react quickly to feedback, and consistently deliver work that is easy for us to approve and move forward with. We’ve been happy to give them more ownership because the quality of their work gives us confidence in their decisions.

I'm impressed by how flexible Pragmatic Coders is (...). Culturally, they're a really good fit for us, and the team is very responsive to feedback. Whenever I ask them to do something, they look at it, and they're not scared to push back. I've found it very easy to work with them — we have more of a partnership than a client-supplier relationship.

Pragmatic Coders pay attention to detail and understand the business domain correctly. They led us to a successful launch of our product this year. We’re happy with the effects of their work. Our team is still using the platform and building on top of it.

The entire focus was on the product and the customer, and I loved it. (...) The team was turning up with solutions to problems I didn't know we had.

It’s truly been a partnership. They have an in-depth understanding of our client base and what services we provide, anticipating evolving needs and addressing them by adding new features into our system. Their team also makes sure that there is a shared understanding so that what they deliver meets my organization's and our clients’ expectations.

(...) Pragmatic has highly skilled engineers available immediately but most importantly, passionate people who love what they do and learn new things very quickly. I recommend Pragmatic Coders to anyone who requires expert software development no matter the stage of their business.